What is a Bill of Lading?

By admin

/ March 19, 2024

In the dynamic realm of international trade, the ‘bill of lading’ holds a pivotal role in ensuring the smooth transportation…

Read More

By Ansh Agarwal, Researcher, NITISARA

Driven by Vision 2030 and the UAE’s Operation 300bn, Middle Eastern nations are investing over $130 billion into logistics infrastructure, energy transition, and industrial localization. According to Agility’s 2024 Emerging Markets Logistics Index, GCC countries climbed 5–7 positions in global rankings, signaling a shift from import dependency to self-reliance. With EV-ready logistics parks, digital freight corridors, and strategic storage of critical materials underway, resilient and green supply chain logistics are becoming the backbone of economic diversification. This blog explores how Gulf economies are addressing vulnerabilities, scaling local supplier ecosystems, and embedding sustainability into the logistics value chain.

The Middle East stands at a pivotal moment in its economic and industrial evolution. With Vision 2030 and similar national agendas gaining momentum across the Gulf, regional governments are accelerating efforts to diversify away from oil dependency, modernize infrastructure, and build future-proof economies. This transformation is being driven not only by demographic shifts such as the rise of younger, highly educated populations and increasing female workforce participation but also by the urgency to withstand post-pandemic shocks, geopolitical volatility, and climate-driven disruptions. In this context, building resilient and localized supply chains has become a strategic imperative, not just a policy aspiration.

Countries like Saudi Arabia, the UAE, and Oman are investing billions into supply chain transformation through localization mandates, supplier development initiatives, renewable energy zones, and smart logistics infrastructure. Saudi Arabia’s IKTVA program, for example, has pushed local content in procurement from less than 20% to over 60% across key sectors in under a decade. Meanwhile, the UAE’s National In-Country Value (ICV) program saw $13 billion redirected into the local economy by the end of 2023 alone. At the heart of these shifts is a recognition that resilient, green supply chains are foundational to economic sovereignty, industrial innovation, and long-term competitiveness in the global marketplace. This blog explores the strategies, policy frameworks, and technological levers reshaping supply chain logistics in the Middle East today.

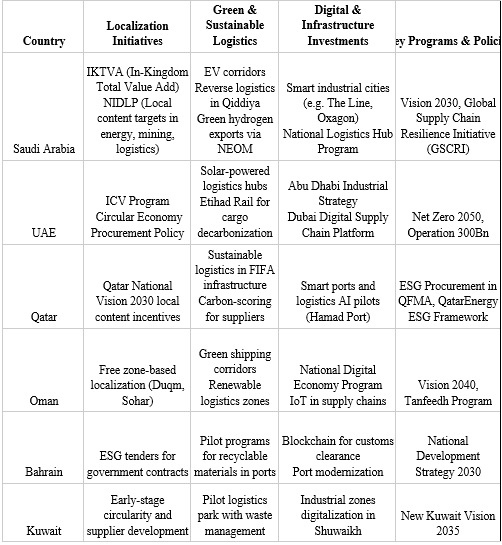

Localization is no longer just a policy buzzword in the Gulf, it is central to national transformation agendas. Saudi Arabia’s Vision 2030, the UAE’s Operation 300bn, and Oman’s Vision 2040 all emphasize local content development to reduce import dependency, expand domestic industries, and stimulate private sector participation. For instance, Aramco’s IKTVA program now requires suppliers to meet strict local value creation benchmarks, helping grow a local supplier base that supports not only oil and gas but also chemicals, metals, and construction. Similarly, ADNOC’s ICV framework influenced over AED 44 billion ($12 billion) in procurement spending in 2023 alone, creating ripple effects across UAE’s manufacturing and services sectors.

However, while national champions like SABIC, ADNOC, and Oman Mining Company are pushing forward, many localization efforts still face friction at the operational level. Challenges include a shortage of skilled local vendors, unclear localization metrics, and uneven digital maturity across suppliers. Procurement guidelines often favor stated LC targets over realized outcomes, and follow-up mechanisms remain inconsistent across agencies. Moreover, cross-border projects struggle with differing standards and fragmented local ecosystems. To bridge these gaps, companies are adopting more proactive supplier development strategies, prequalifying vendors with LC thresholds, co-investing in skills training, offering price preferences for domestic suppliers, and incorporating carbon scoring into tender evaluations. When done right, this transforms localization from a compliance burden into a tool for innovation, value creation, and regional resilience.

GCC National Supply Chain Transformation Matrix

Resilient and sustainable logistics infrastructure is pivotal to the Gulf’s transition from hydrocarbon dependence to diversified industrial economies. Ports like Jebel Ali, King Abdulaziz Port, and Sohar are evolving into smart logistics hubs, integrating AI-powered tracking, cold chain systems, and customs digitalization to enhance throughput and reduce inefficiencies. Saudi Arabia’s National Transport and Logistics Strategy aims to position the Kingdom as a global logistics hub, targeting a 30% modal shift to rail and increasing the sector’s contribution to GDP to 10% by 2030. The UAE, similarly, has launched a $3 billion National Rail Network (Etihad Rail), aiming to reduce freight emissions by 70–80% compared to trucks, while supporting inland logistics zones and free trade corridors.

To embed resilience into these systems, regional governments are investing in circular logistics models. For example, NEOM’s The Line and Oxagon integrate underground logistics networks and EV-powered freight systems to reduce surface congestion and emissions. In Oman’s Duqm and Sohar SEZs, reverse logistics and material reuse strategies are being piloted to enhance construction circularity. Major logistics players like Aramex and Agility are also introducing carbon-neutral warehousing, electrified last-mile fleets, and blockchain-based inventory tracking. These efforts help mitigate risks from global shocks be it Suez Canal blockages, pandemics, or geopolitical tensions by enabling faster rerouting, local buffer stocks, and digitally orchestrated flows. The result: shorter, greener, and smarter supply chains that strengthen economic continuity and position the Gulf as a trade and transit nexus between Asia, Africa, and Europe.

As Gulf countries deepen industrial diversification, the development of renewable energy supply chains has emerged as a strategic priority. While global supply chains, particularly from China, still dominate solar and wind components, Saudi Arabia, the UAE, Oman, and Qatar are investing in domestic capabilities to reduce import reliance. Saudi Arabia aims to localize up to 75% of its energy sector by 2030, with initiatives like Desert Technologies and Alfanar already manufacturing solar and wind components. Meanwhile, the UAE pursues a flexible, trade-driven model, complemented by investments in African mining to secure raw materials.

Oman and Qatar are incentivizing local production through special economic zones and upstream investments in polysilicon and critical minerals. However, challenges persist: limited skilled workforce, fragmented market size, and high production costs. To overcome this, experts emphasize regional integration, pooling demand, standardizing procurement, and enabling joint investments in midstream manufacturing and workforce training. A GCC-wide renewable supply chain strategy could serve as both an economic enabler and a geopolitical hedge.

As the GCC transitions from oil-centric economies to diversified industrial powerhouses, supply chain resilience is no longer optionalit is foundational. Whether through supplier localization, digital infrastructure, or renewable manufacturing ecosystems, countries must adopt integrated strategies to weather future shocks and reduce external dependency. GCC leaders, businesses, and OEMs that embed localization, circularity, and green energy into logistics and production will be best positioned to lead. The convergence of Vision 2030-style reforms with global supply chain volatility presents a historic opportunity. Seizing it will require regional collaboration, transparent measurement, and targeted investment but the payoff is a future-proofed, self-reliant Gulf economy ready to lead on the world stage.

The views expressed do not represent the company’s position on the matter. Stay informed through Nitisara Platform and Blogs and adapt to emerging trends are poised to thrive in the competitive global marketplace. – https://nitisara.org/category/blogs-updates/

References:-