What is a Bill of Lading?

By admin

/ March 19, 2024

In the dynamic realm of international trade, the ‘bill of lading’ holds a pivotal role in ensuring the smooth transportation…

Read More

By Kanak Kansal, Researcher, Nitisara

In emerging markets, about 70% of formal jobs come from SMEs. Yet, they continue to face significant financial constraints, with the global SME credit gap estimated at a staggering $5.7 trillion, reflecting a profound mismatch between enterprise potential to export/expand and access to capital. This article elucidates on the funding challenges faced by SMEs globally and the policies and incentives available for them as possible solutions.

Even with their entrepreneurial spirit, SMEs frequently lack the size, networks, and means of large exporters. Entry costs into markets, technical barriers, foreign regulatory standards not known to them, and absence of brand names are obstacles to their access to global opportunities. Many international organisations across the world are working to smoothen the herculean task of financing for SMEs. For example, the International Labour Organization (ILO) aims to develop new and context-specific approaches to address current and future challenges faced by MSMEs across the globe, in particular towards creating a conducive business environment which impacts positively on MSMEs’ productivity and competitiveness as well as their capacity to create decent and productive work. Also, the World Bank Group also offers advisory and lending services to clients to increase the contribution that SMEs can make to the economy including underserved segments such as women owned SMEs. We analysed a worldwide overview of significant export promotion programs for SMEs, such as financial support, online trade platforms, intellectual property protection, and capacity-building interventions.

Small and Medium Enterprises (SMEs) form the backbone of the global economy, accounting for over 90% of businesses and more than 50% of employment worldwide. Despite their scale and significance, SMEs face a persistent financing gap estimated at over USD 5 trillion annually, according to the International Finance Corporation (IFC). This gap is especially acute in the Global South, where SMEs play a critical role in supply chains for textiles, agriculture, electronics, and processed foods, yet struggle to access affordable capital due to weak financial infrastructure, limited collateral, and policy asymmetries. The financing gap is not just a domestic policy issue; it lies at the intersection of international development governance and trade regulations, making it a global development challenge. As SMEs increasingly integrate into cross-border value chains, their under-financing not only stifles local growth but also creates vulnerabilities in global supply chain resilience. Bridging this gap requires coordinated global governance models, combining multilateral trade reforms, blended finance strategies, and MSME-centered credit innovations to ensure more inclusive and sustainable trade systems.

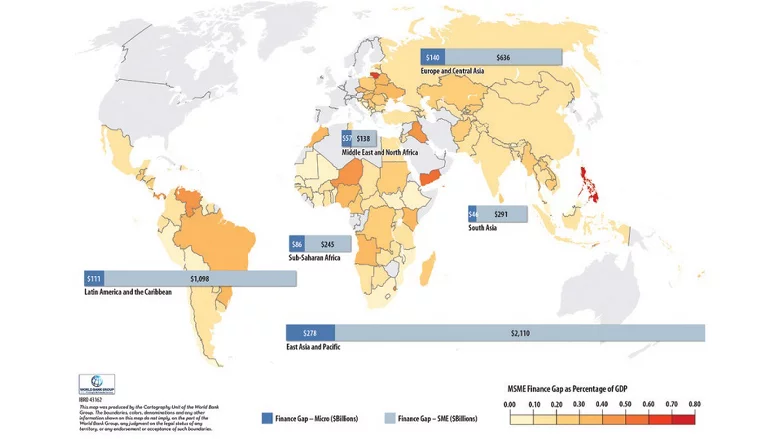

This map illustrates the global distribution of formal SME financial gaps, highlighting the significant disparities in access to finance across regions.

Figure 1. Illustration of formal SME financial gaps in different countries Source: https://www.worldbank.org/en/topic/smefinance

SMEs are less likely to be able to obtain bank loans than large firms, instead they rely on internal funds, or cash from friends and family, to launch their enterprises, but it remains a highly unstructured financing model. The table below represents the unmet financing need of $5.2 trillion of MSMEs annually on a global level, as estimated by the International Finance Corporation (IFC).

| METRIC | VALUE / REGION |

| Total number of MSMEs with unmet financing need | 65 million firms |

| Share of formal MSMEs in developing countries with unmet need | 40% |

| Total annual financing gap | $5.2 trillion |

| Gap compared to current global MSME lending | 1.4 times |

| REGIONAL SHARE OF GLOBAL FINANCE GAP | |

| East Asia & Pacific | 46% (largest share) |

| Latin America & Caribbean | 23% |

| Europe & Central Asia | 15% |

| FINANCE GAP AS % OF POTENTIAL DEMAND (BY REGION) | |

| Latin America & Caribbean | 87% |

| Middle East & North Africa (MENA) | 88% (highest proportion) |

| Share of formal SMEs without access to formal credit | ~50% |

| Finance gap with informal & micro enterprises included | Increases significantly |

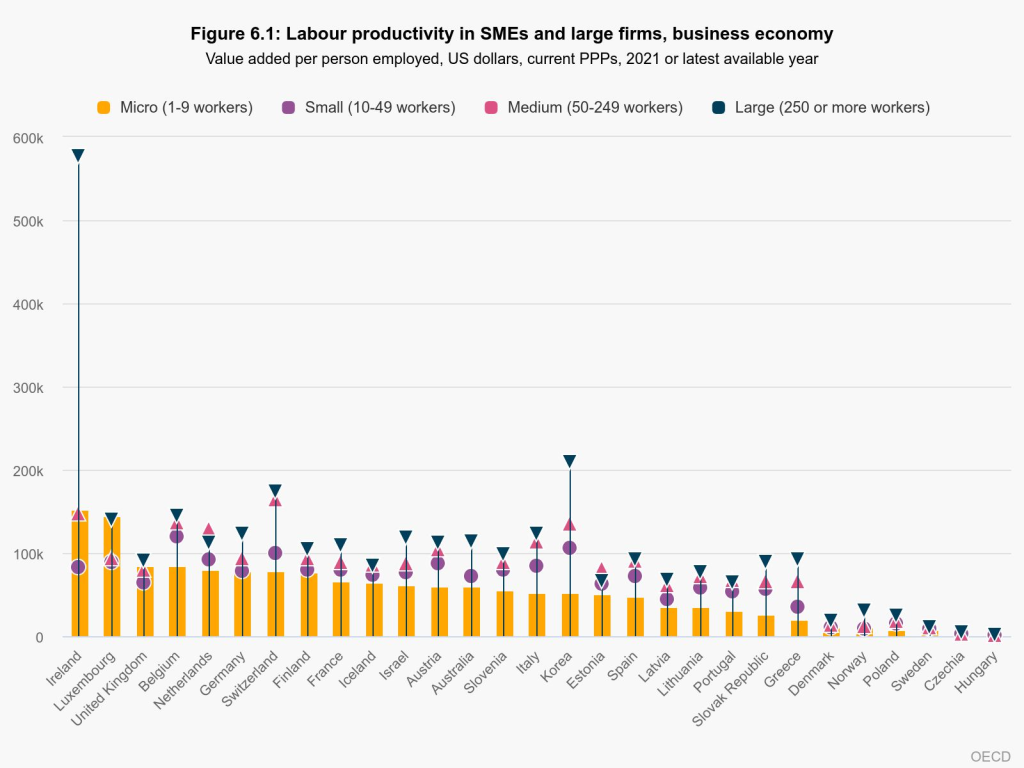

Figure 2. Labour productivity in SMEs and large firms, business economy (2021), Source: https://www.oecd.org/en/topics/sme-indicators-benchmarking-and-monitoring.html

Larger firms consistently offer higher average wages compared to micro and small enterprises across most countries. This wage gap is especially wide in nations like Ireland, Korea, and Switzerland. In contrast, Eastern European countries show lower wages across all firm sizes. Overall, firm size has a strong positive correlation with wage levels.

Labour productivity in SMEs is lower because of a number of interconnected issuesOne of the key drivers is restricted access to funding, which hinders SMEs from investing in advanced equipment, technology, and digital capabilities that have the potential to greatly improve efficiency. In contrast to larger corporations, SMEs frequently use old equipment and hand-held systems, contributing to slower rates of production and less output per employee.

Robust monetary and fiscal support mechanisms are essential to maintain SME export activity. Monetary efforts, usually supported by central banks and donor governments, comprise concessional credit lines, refinancing programs, and liquidity injections intended to facilitate access to finance for small firms. Fiscal aid usually consists of tax exemptions, loan guarantees, credit guarantee funds, and direct subsidies. Germany, India, Nigeria, and Malaysia have been shown to illustrate the effect of the confluence of financial inclusion policies and digital infrastructure. Development banks such as SIDBI in India or KfW in Germany tend to act as intermediaries for providing such credit facilities, while global institutions such as the World Bank and IFC co-finance or provide guarantees for SME loans to de-risk lending. These interventions consolidate the financing ecosystem and enable SMEs to participate in international trade confidently.

| Country / Region | Scheme / Institution | Scale & Duration | Key Features |

| Chile, China, Hungary, Poland, Thailand, Malaysia | Central bank funded SME credit lines | From 0.5% up to ~14% of GDP | Concessional rates, multi-year tenor, loan expansion-linked caps |

| Jordan | World Bank credit line (~$70M + $50M) | 2010s onwards, ~8,149 MSMEs financed | 58% outside capital; strong outreach to women & youth |

| Nigeria | Development Bank of Nigeria via World Bank | ~$243.7M disbursed to ~50,000 MSMEs | 70% women recipients |

| India | SIDBI line of credit ($500M + $265M) | 2020s ongoing; includes Fund-of‑Funds ($1.5B by 2025), $1.9B private leverage | Digital lending via “contactless” aggregator |

| Country / Region | Program | Scale | Description |

| Germany (KfW) | KfW SME Loans | > €3B ongoing since 1971 | Long‑term credit via banks with capital‑market refinancing |

| Italy | Fondo di Garanzia | Guarantees covering €17B → €32B new loans | Up to 80% guarantee on SME loans |

| Ireland | SBCI credit line | €4B (2014–18) | On‑lending via banks, improves cost & flexibility |

| Spain | ICO lending facility | €2–7B per year since 1993 | Target: fixed asset investment with grace periods |

| UK | Funding for Lending Scheme | ~£80B at launch (2012–15) | Incentivized SME lending via subsidized Treasury bills |

| Western Balkans (EFSE, WBIF) | Micro & SME credit + guarantees | €109.9M EU grants → €3–4B lending | Reduced interest, collateral, green/digital focus |

| Italy, Poland, Spain, UK, France | Tax incentives (EMTR reductions) | 1–10% lower tax | SMEs enjoy lower effective marginal tax rates |

| IFC / We-Fi | Gender-lens SME finance | $48B global SME finance; $1.6B to women-led | 196 projects, 43 countries + $69M We-Fi grant |

Digital platforms are rapidly emerging as cost-effective gateways for SMEs to access international markets. Private initiatives such as Amazon Global Selling, Alibaba, and eBay offer tailored onboarding support to help small businesses tap into global demand. Governments are also stepping up with targeted programs, for instance, Malaysia’s MATRADE eTrade Program and India’s ONDC B2B export module aim to digitize export processes for SMEs by subsidizing listing costs, offering onboarding assistance, and facilitating logistics support. Digital learning tools are playing a pivotal role in enhancing SMEs’ export readiness. Platforms like the International Trade Centre’s SME Trade Academy and the WTO’s e-Learning portal offer free, multilingual courses on key topics such as export compliance, customs documentation, and international e-marketing. In many countries, governments now mandate online certification to qualify for export incentives, ensuring that SMEs are well-versed in global trade procedures and equipped to navigate the complexities of cross-border commerce.

| Platform / Program | Launched By | Year of Launch | Key Initiatives / Features |

| Amazon Global Selling | Amazon (Private) | 2015 | Onboarding support, global marketplace access, logistics and warehousing (FBA) |

| Alibaba.com | Alibaba Group (Private) | 1999 (revamped for SMEs in 2017) | Global B2B sourcing, trade assurance, seller training programs |

| eBay Global Selling Program | eBay (Private) | 2004 (India relaunch in 2019) | Cross-border listings, simplified shipping, seller protection |

| MATRADE eTrade Program | Govt. of Malaysia | 2014 | Listing subsidies, onboarding, export readiness support on platforms like Alibaba & eBay |

| ONDC B2B Export Module | Govt. of India | Pilot in 2024 | Digital infrastructure for SME exports, listing support, logistics integration |

| ITC SME Trade Academy | International Trade Centre | 2014 | Free multilingual e-learning courses on trade procedures and digital marketing |

| WTO e-Learning Platform | World Trade Organization | 2002 | Online courses on trade policy, export rules, and trade facilitation |

| Figure 4: Phase 1 of MATRADE’s eTRADE generated RM 300M in export sales for SMEs, while Phase 2 has generated RM 127M so far. | Figure 5: As of 2024, 70% of sellers on India’s ONDC platform were SMEs, reflecting the initiative’s success in grassroots digital onboarding. |

The views expressed do not represent the company’s position on the matter. Stay informed through Nitisara Platform and Blogs and adapt to emerging trends are poised to thrive in the competitive global marketplace. – https://nitisara.org/category/blogs-updates/